This post was originally published on this site

A strong dollar isn’t the bearish omen it used to be.

That’s good to know, since the U.S. Dollar Index

DXY,

has strengthened over the past year — up 14%, according to FactSet. Some on Wall Street are worrying because on past occasions a strong dollar was followed by an earnings recession.

Those worrywarts are living in the distant past, according to an analysis I conducted of the dollar index’s relationship to corporate earnings. It is true that, several decades ago, a stronger dollar was more often than not followed by lower corporate earnings. But in more recent decades, that pattern has largely disappeared.

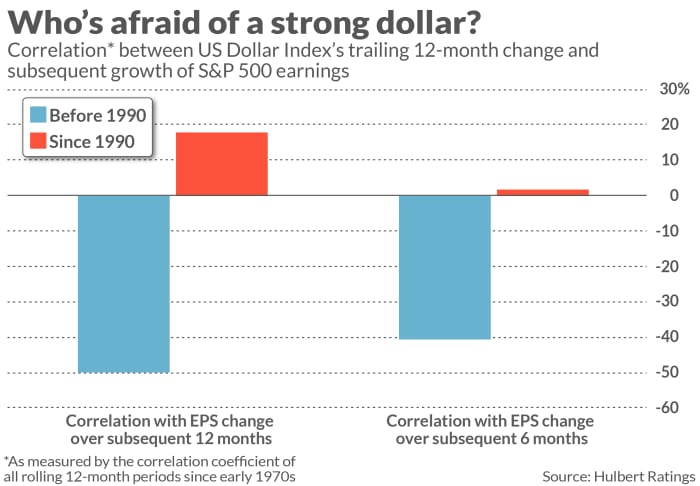

This is evident in the accompanying chart, above, which reports the correlation between the dollar index and the S&P 500’s

SPX,

EPS growth rate over the subsequent six- and 12-month periods. The coefficient’s theoretical range is from minus 1 (which would be the case if dollar strength was always followed by EPS weakness, and vice versa) to plus 1 (which would be the case if strength was followed by strength and weakness by weakness). A coefficient of 0 would mean there is no detectable relationship between the two.

Notice that, prior to 1990, there was a significant inverse correlation between the dollar and subsequent earnings growth. Since then, the correlation has been weakly positive. While the pre-1990 inverse correlations were statistically significant, the post-1990 correlations are not significant at the 95% confidence level that statisticians often use when determining if a pattern is genuine.

What happened? One big change is that companies have become much more internationally diversified and better at managing their foreign currency exposure. Consider a hypothetical firm that receives much of its revenue from overseas sales (denominated in foreign currencies) but whose production is located in the U.S. (denominated in U.S. dollars). Such a firm’s earnings would indeed be vulnerable to a stronger dollar, since the dollar equivalent of its foreign sales would be lower.

But how many firms actually come close to this hypothetical extreme? While some may have come close several decades ago, this is not generally the case currently. U.S.-based multinational firms have exported much of their production to outside the U.S., so their expenses and revenues both fluctuate as the dollar strengthens and weakens — largely offsetting each other. And, to the extent that a firm continues to have lopsided currency exposure, either on the revenue or expense side of its ledger, it will hedge that exposure with currency futures or other derivatives.

The implication of this analysis is that the U.S. dollar’s strength does not pose a particular threat to corporate earnings or, in turn, the S&P 500 or other U.S. stock market indices. This doesn’t necessarily mean that equities will rally in coming months; it just means that, if the market falls, you can’t blame the strong dollar for causing it.

So don’t sweat the dollar’s strength. If you want to worry about something, find something else.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com.

Hear from Ray Dalio at MarketWatch’s Best New Ideas in Money Festival on Sept. 21 and 22 in New York. The hedge-fund pioneer has strong views on where the economy is headed.